I’m often on the search for the thoughts of others on self-reliance. One time the search engine showed me an article by Darius Foroux. I’ll probably get to that one at a later date, but in the process I ended up reading another of his articles which I also found quite interesting. In it he proposes that the purpose of life is not happiness, but usefulness. This may sound familiar; it was posited by Ralph Waldo Emerson:

“The purpose of life is not to be happy. It is to be useful, to be honorable, to be compassionate, to have it make some difference that you have lived and lived well.”

Foroux expands on this:

Most things we do in life are just activities and experiences.

You go on holiday. You go to work. You go shopping. You have drinks. You have dinner. You buy a car.

Those things should make you happy, right? But they are not useful. You’re not creating anything. You’re just consuming or doing something. And that’s great.

Don’t get me wrong. I love to go on holiday or go shopping sometimes. But to be honest, it’s not what gives meaning to life.

What really makes me happy is when I’m useful. When I create something that others can use. Or even when I create something I can use.

He goes on to explain that it’s what we are doing each day, in large or small ways, to make a difference is what life is all about. Whether it’s taking on a little extra work, unasked, for your boss, writing an article sharing something important you’ve learned, or building a piece of furniture, it’s all useful in some way to someone. It’s nothing big, necessarily, but a life built out of these small things adds up to a what we could consider “a good life.” Or, as Thoroux puts it:

The last thing I want is to be on my deathbed and realize there’s zero evidence that I ever existed.

He’s not advocating changing the world in any big way, necessarily. Just do something a little outside yourself, a little more permanent:

One day I woke up and thought to myself: What am I doing for this world? The answer was nothing.

And that same day I started writing. For you, it can be painting, creating a product, helping the elderly, or anything you feel like doing.

I think his last piece of advice must have been aimed directly at me:

Don’t take it too seriously. Don’t overthink it. Just DO something that’s useful. Anything.

I recently came across an address by Robert D. Hales that shared valuable insights into money and how we perceive it. I thought I’d share some of it here.

All of us are responsible to provide for ourselves and our families in both temporal and spiritual ways. To provide providently, we must practice the principles of provident living: joyfully living within our means, being content with what we have, avoiding excessive debt, and diligently saving and preparing for rainy-day emergencies.

…

How then do we avoid and overcome the patterns of debt and addiction to temporal, worldly things? May I share with you two lessons in provident living that can help each of us. These lessons, along with many other important lessons of my life, were taught to me by my wife and eternal companion. These lessons were learned at two different times in our marriage—both on occasions when I wanted to buy her a special gift.

The first lesson was learned when we were newly married and had very little money. I was in the air force, and we had missed Christmas together. I was on assignment overseas. When I got home, I saw a beautiful dress in a store window and suggested to my wife that if she liked it, we would buy it. Mary went into the dressing room of the store. After a moment the salesclerk came out, brushed by me, and returned the dress to its place in the store window. As we left the store, I asked, “What happened?” She replied, “It was a beautiful dress, but we can’t afford it!” Those words went straight to my heart. I have learned that the three most loving words are “I love you,” and the four most caring words for those we love are “We can’t afford it.”

The second lesson was learned several years later when we were more financially secure. Our wedding anniversary was approaching, and I wanted to buy Mary a fancy coat to show my love and appreciation for our many happy years together. When I asked what she thought of the coat I had in mind, she replied with words that again penetrated my heart and mind. “Where would I wear it?” she asked. (At the time she was a ward Relief Society president [ed. leader of the church’s women’s charity auxiliary] helping to minister to needy families.)

Then she taught me an unforgettable lesson. She looked me in the eyes and sweetly asked, “Are you buying this for me or for you?” In other words, she was asking, “Is the purpose of this gift to show your love for me or to show me that you are a good provider or to prove something to the world?” I pondered her question and realized I was thinking less about her and our family and more about me.

After that we had a serious, life-changing discussion about provident living, and both of us agreed that our money would be better spent in paying down our home mortgage and adding to our children’s education fund.

These two lessons are the essence of provident living. When faced with the choice to buy, consume, or engage in worldly things and activities, we all need to learn to say to one another, “We can’t afford it, even though we want it!” or “We can afford it, but we don’t need it—and we really don’t even want it!”

My wife has often been my backstop on financial issues, questioning the criticality of some of my desired purchases. I may not always have appreciated it at the time, but I do appreciate her keeping me grounded. I’m grateful for the partnership we’ve built through the years around managing our money. I do the bulk of the management and bill-paying, and she the bulk of the household shopping. This works well primarily because we share the same goals and we continually communicate.

Of course you don’t need a significant other to establish and maintain financial discipline. One of the key skills is to learn to distinguish between needs and wants, and when considering wants, understanding the root of that want. Developing the ability to police yourself and say, “I may not want this thing for the right reasons” is invaluable.

The bottom line with money is that either we learn to master it, or our money will become our master–or rather, those to whom we end up owing money. The more control we gain over our finances the greater freedom we will enjoy.

There is a curse of uncertain origin: “May you live in interesting times.” Well, it would appear we are cursed. Within the space of a few months we’ve experienced a pandemic with its accompanying challenges, Asian murder hornets, and now civil unrest and riots. And through it all we’ve experienced a constant social media barrage as seemingly everyone feels qualified and obligated to tell us what to do, what to think, and what to feel.

It’s difficult to not just turn off the light and go back to bed, to say nothing of meeting each day with a smile. There’s few things more annoying to me when I’m already stressed than to have everyone lecturing one another and looking to find fault. I prefer to make social media my “happy place,” but lately it’s been anything but.

The things is, my life isn’t that bad. Working from home isn’t as difficult as I’d feared. I’m still getting paid. I’ve got most of my family around me, and my distant daughter is safe. My wife and son kept their jobs throughout all this. We’ve been able to hold church at home. I don’t really care that much about going places–at least places that would now be off limits. Our house is comfortable, our yard is perking up nicely, and I have plenty of cute, furry things to pet when I need a little fur-therapy.

But even with all that some days it’s just been almost too much to bear. Even without everything going on right now life can still hit you hard on an off day. Now, there are people who deal with anxiety and depression, and I by no means imply they should be able to just snap out of it, or that anything I’m about to suggest should work for them. But for the rest of us, here are a few things I’ve found helps me cope.

Exercise – I realized at one point amid my home isolation I had let my exercise program slide. Even when I was doing it I wasn’t doing it for very long. So I changed things up, getting up a little earlier to make sure I was getting longer, regular activity. I also took advantage of my being home and my shared interest with my younger son to get outside every other afternoon for some basketball. Pretty soon I noticed two improvements. I was feeling better physically from improved health, and following through on my goal was boosting my general satisfaction with myself.

To Do Lists – This probably won’t work for everyone, but in my case the less I feel I accomplish the worse I feel about myself. I actually don’t like to-do lists, but I do like the feeling I get when I check off an item or when I review my accomplishments at the end of the week. The thing that surprised me was to find that the size of the task doesn’t matter so much. If it’s something you need to remember to do, put it on there–in fact, the smaller they are, the easier it is to do them, so if you have something big that can be broken down into smaller tasks (ie. getting stuff you need, prep-work, the actual job, cleanup, etc.), do it! You’ll have concrete proof of having done something, and it really helps.

Ditch the Downers – I have a love-hate relationship with social media. When the majority of my feed is positive I feel positive. But the more negativity that creeps in the more I feel myself absorbing it. And I hate unfriending people–my problem, I know. But recently I discovered that Facebook gives you the ability to “snooze” people for 30 days rather than unfriending or hiding them. I find it much easier to hit the “smite” button and say, “I don’t want to deal with you right now.” There may be other ways, including taking a break altogether. If you’re like me and you can’t help absorbing the negative energy, it’s okay to admit you just can’t handle it. You shouldn’t have to handle it. Most people wouldn’t come over to your house to act like that, so it’s okay to avoid them online if necessary. Take a break.

It’s Okay – Related to the previous point, I can really get on myself sometimes. I keep telling myself I have no reason to be feeling the way I feel, that other people don’t feel this way, and that I should just snap out it and move on. Sometimes I can do it, but sometimes I just can’t. And I’m slowly coming to realize that’s okay! It’s okay to feel what I’m feeling. It might be good to look more closely and see what might be behind it, but ultimately…it’s okay. Also, cut other people some slack. We all deal with things differently, and things that bother me won’t necessarily bother you–and vice versa. If I’m dealing with something, chances are you’re dealing with something too. It’s okay if you don’t handle it the way I would. I don’t need to be like you in how you handle things. People get angry, get stressed, get hard to live with. Let them. Give them some distance if you can’t handle it yourself, but don’t beat yourself up over it. Own how you feel and make a plan to move forward.

Pull a Scarlet O’Hara – Years ago when I was out of work for two years I would have the occasional meltdown. My poor wife couldn’t talk any sense into me, and I most certainly couldn’t talk myself out of it. I’d get caught in circular thinking and go down in flames. Eventually I started learning that some days I’d just have to surrender and go to bed early. Almost without fail things would look better the next day. A good night’s sleep can act as a reset button, clearing out the mental garbage you couldn’t get rid of the day before. Sometimes I’ve even found the admission that I just can’t handle it to be cleansing enough to turn things around.

Get Outside – During this pandemic that option hasn’t been available to everyone, but even just getting out for a while to walk the dog can be great. A change of scenery works wonders sometimes.

Well, that’s the extent of my wisdom. Just remember, free advice is worth every penny you pay for it! But hopefully something in here may just help. Everyone struggles from time to time. We’ll get through it sooner or later, but every little tool, every strategy helps.

What are some of your favorite coping strategies? Leave a comment!

About a month ago I began discussing an article from Wikihow.com on “4 Ways to Be Self Reliant,” by Trudi Griffin, LPC, MS. The article is more about relationships than what I would consider self-reliance, but she still makes some valid points. Today I want to look at her second point, managing money independently. She breaks money management down into six areas:

Learn how to manage money

Get out of debt

Pay cash instead of using your credit card

Keep cash on hand at all times

Own a home

Live within your means

To begin with Griffin warns against allowing others to manage your money. I agree with her basic premise, that you can lose your independence if you lost control of your money, but that depends on the nature of your relationship with that person. In most marriages one of the two usually assumes responsibility for managing the money. If you are good at communicating, have compatible financial goals, and trust one another it’s actually easier to have one partner take primary responsibility and keep the other informed. Her second concern is more valid: if the primary money manager is unable to continue in that role it may be very difficult for the other partner to step in. Even if you are not the money manager in your relationship, make sure you know how to access everything and are comfortable managing money yourself.

Griffin also encourages everyone to get out of debt, though what she really focuses on is keeping your debt manageable. According to her, your total long-term debt payments (mortgage, auto and school loans, and credit card debt) shouldn’t exceed 36% of your monthly income. If your debt payments exceed this level you should make every effort to get that debt load paid down as quickly as possible.

As a corollary to that, Griffin also advocates paying cash for everything, and to keep cash on hand (and in savings) at all times. This seems primarily to be to keep your credit card debt low, and I somewhat agree with this. If you have difficulty paying off your credit cards, or can’t resist charging more money on them, then by all means you should avoid using those credit cards. But if you have developed financial discipline and never miss making your payments because you’re able to set money aside to make those payments, there may be a way to make your credit cards work for you.

I recently read I Will Teach You To Be Rich, by Ramit Sethi. The man has some good ideas about acquiring, building, and managing wealth–and some ideas I’m less keen on. But one suggestion he makes is to put your regular expenses, as much as possible, on your credit cards and then set that money aside to pay the bill off quickly. If you get the right credit card you can earn travel miles or cash back rewards that amount to free money. I’m disciplined with managing my budget, and so I decided to try it. I haven’t put as much on my card as I could, but already within the past several months I’ve picked up nearly $250 of cash back rewards. It’s free money. But if you’re not so good at managing your credit card debt and paying off your account monthly, it’s best to follow Griffin’s advice and avoid credit cards altogether.

Griffin’s next suggestion is to own a home. I’m not as sure about this one as I once was. Right now interest rates are low, so you may only pay about 50% more than the cost of your house in repaying the loan. Depending on how long you live there, the value of the home may increase well beyond that. Our first house did just that. But you don’t always control how long you live somewhere these days. We had to move when I lost my job ten years ago, and the timing was terrible–the housing market had collapsed and I owed considerably more on that house than I could sell it for.

There’s also the maintenance costs and hassle of a house to consider. So far since moving into our house nine years ago we’ve replaced the roof, replaced the furnace, air conditioner, and water heater, and bought high-efficiency windows. Granted, that last purchase was voluntary, but that was easily an additional 30-40% the cost of the house we had to find within the first six years of buying it. That, on top of a myriad of other maintenance expenses through the years. If you don’t like or can’t afford doing your own maintenance, or if you can’t be sure how long you’ll be staying where you live, a house may not be the best option. Everyone needs to evaluate their priorities themselves in this area.

Last, but by no means least, we should live within our means. That usually means several things that have to happen. First, you need to know (or learn) exactly how much money you spend each month and where it goes. Second, where at all possible, and perhaps not matter what the sacrifice, you need to adjust your spending to where it is less than what you earn. Third, you need to continually monitor your spending and your justifications for spending and see how you measure up against your budget. You need to be willing and able to adjust your spending to remain below your means–and save the difference religiously.

Frankly, learning how to budget and how to stick to that budget is one of the most important skills one can develop for self-reliance. That’s pretty much the key to achieving financial independence and taking care of “future you.” Or perhaps your spouse and children after you’re gone. Usually in life there are only two choices: either your master your money or your money masters you. Money is seldom a kind master, but it can be a real friend when you learn to master it. Mastering your finances is a key step toward true self-reliance.

The problem with being a free thinker is that it just takes so much more time and effort than just accepting whatever your told. Now, of course I’m saying this tongue-in-cheek, as the cost of not questioning much of what you hear is potentially much, much higher. But in an era when information is available at much higher volumes and speed than any of us can hope to consume, it’s a considerable sacrifice to weigh everything critically.

Take for example the reporting on a recent Gallup poll. I first learned of this poll via an article on a news and opinion site that trends conservative. The headline read thusly:

Gallup Poll Shows That No One Thinks the Media Is Doing a Good Job During the Pandemic

The article cites another article from the Washington Examiner also reporting on the same Gallup Poll, so I went to read the Examiner article. Their headline?

Media botched the virus crisis and made it ‘worse’: Poll

And then I got a novel idea: Let’s go look at the poll itself! There were links, so…why not? Note we are now heading three layers deep. And how do they title the results of their poll?

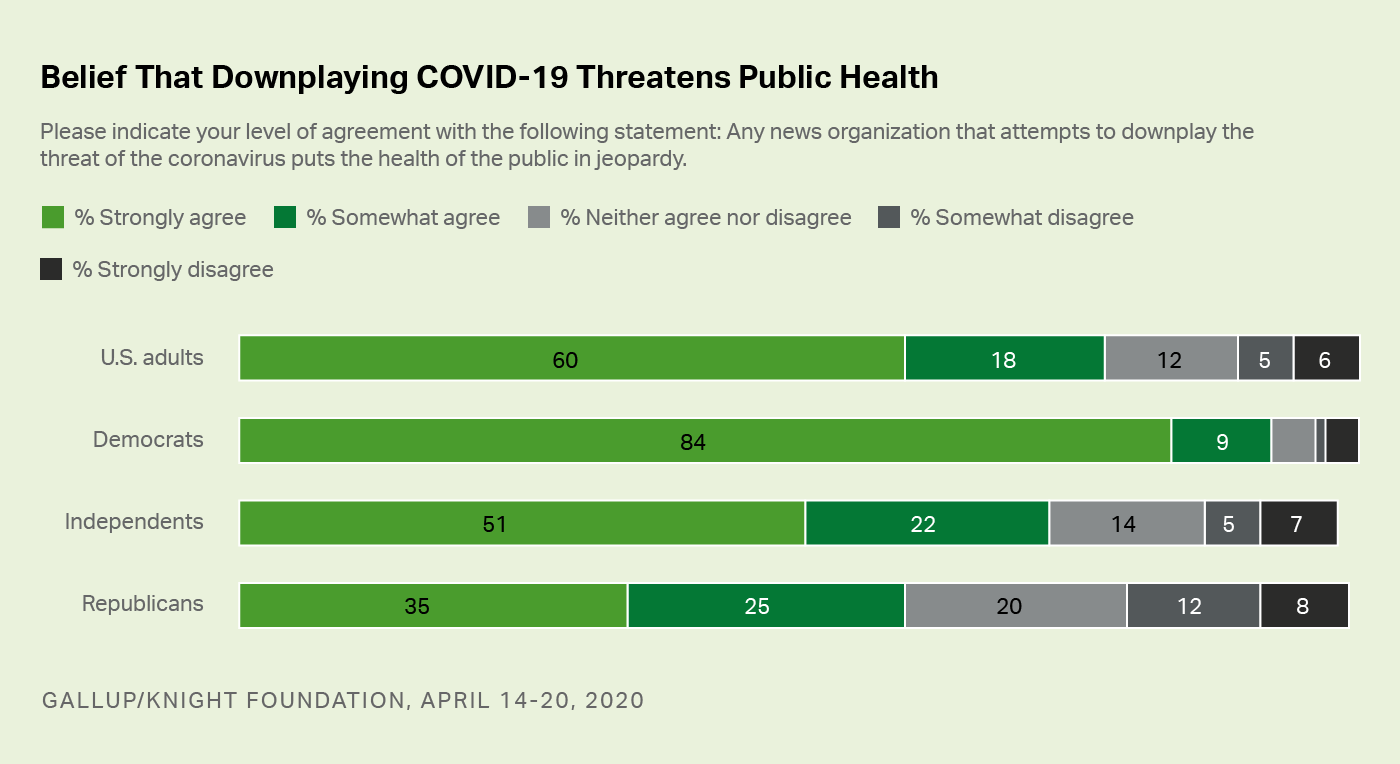

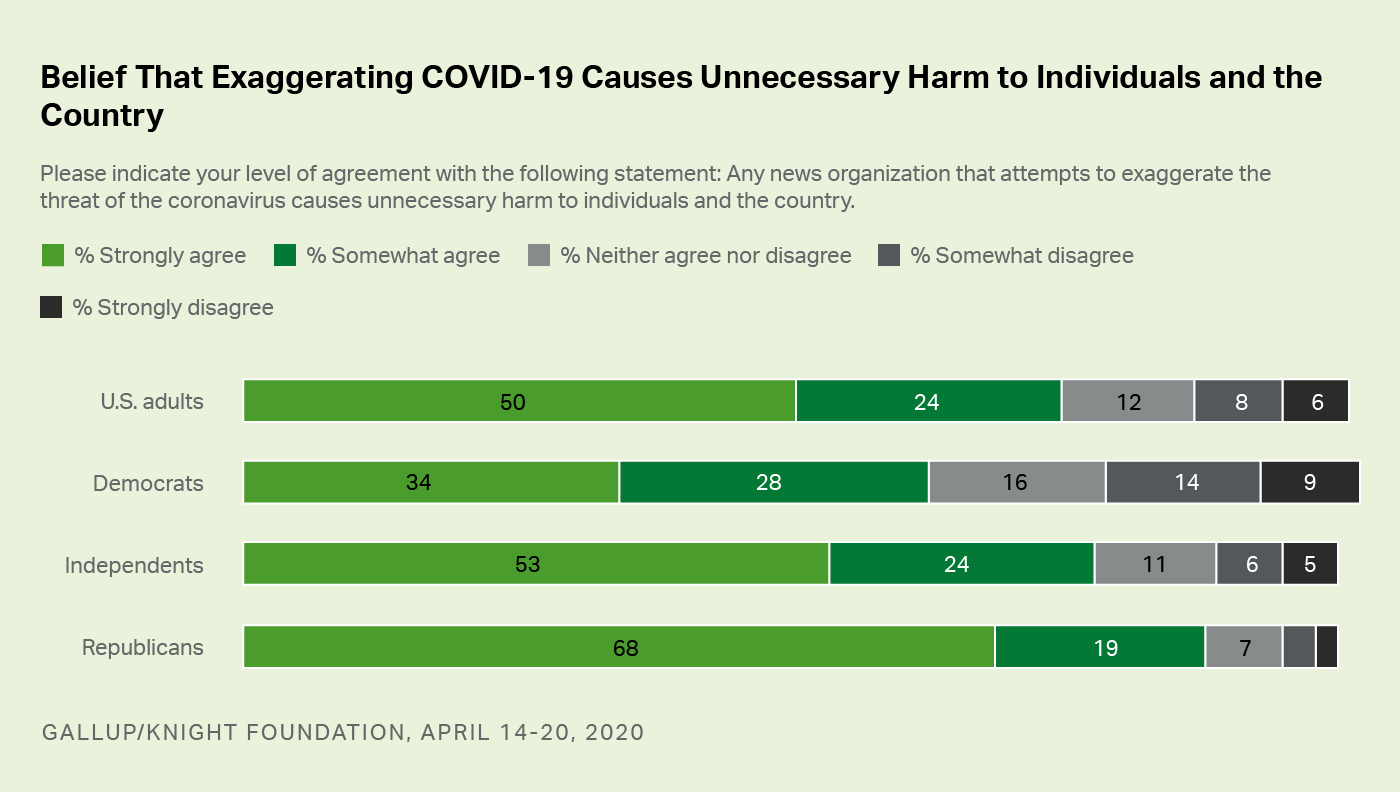

Public Sees Harm in Exaggerating, Downplaying COVID-19 Threat

Following this trail of headlines just by themselves we see the effect of ye olde “Telephone Game.” We somehow went from “over- or under-playing the threat both believed to cause harm” to “The media is doing a poor job.”

But wait, we still haven’t even looked at the actual text of the articles yet. I’m going to ignore the first two and focus in on just the article written around the presentation of the data itself. Here’s their lede:

Media bias is a great concern for Americans, and the implications of such bias for society are magnified when the nation is in crisis, such as the current coronavirus pandemic. A new Gallup/Knight Foundation survey finds that a majority of Americans are concerned about biased news coverage of the coronavirus situation, including reporting that downplays the threat but also reporting that exaggerates it.

Democrats and Republicans diverge on whether exaggerating or downplaying the coronavirus threat is the greater risk. However, they generally agree that the crisis is worse than it needed to be, and that the news media should not wait for the crisis to ease before reporting on official actions that exacerbated the coronavirus situation.

It seems like a pretty good summary. Let’s look at the questions asked and the data obtained and tabulated:

This is as far as the first two articles really get. They focus in on the Republicans vs. Democrats angle, and also on the fact that the majority of all Americans find both exaggeration and down-playing to be harmful. But outside of the data itself, notice something a bit off? They’re asking what they essentially treat as inverse questions, but they word them slightly differently each time. When asking about down-playing they ask if it threatens public health. When they ask about exaggeration, they ask if it causes unnecessary harm to individuals and the country.

Why would they ask them differently? Wouldn’t it make the most sense to ask either “Any news organization that attempts to [down-play/exaggerate] the threat of the Coronavirus causes puts the health of the public in jeopardy” or “Any news organization that attempts to [down-play/exaggerate] the threat of the Coronavirus causes causes unnecessary harm to individuals and the country”? Wouldn’t that make the two questions equally weighted and inverse?

This may be displaying some of my own bias here, but it seems to me that framing the harm in terms of “public health” would tend to grab the interest of Democrats, while framing it in terms of individuals and the country would resonate more with Republicans. I don’t think it’s a coincidence that those groups do tend to rate the harm higher accordingly. Independents, predictably, seem to walk the middle of the road. Could it be this poll was designed to elicit a desired result outside of the stated objective?

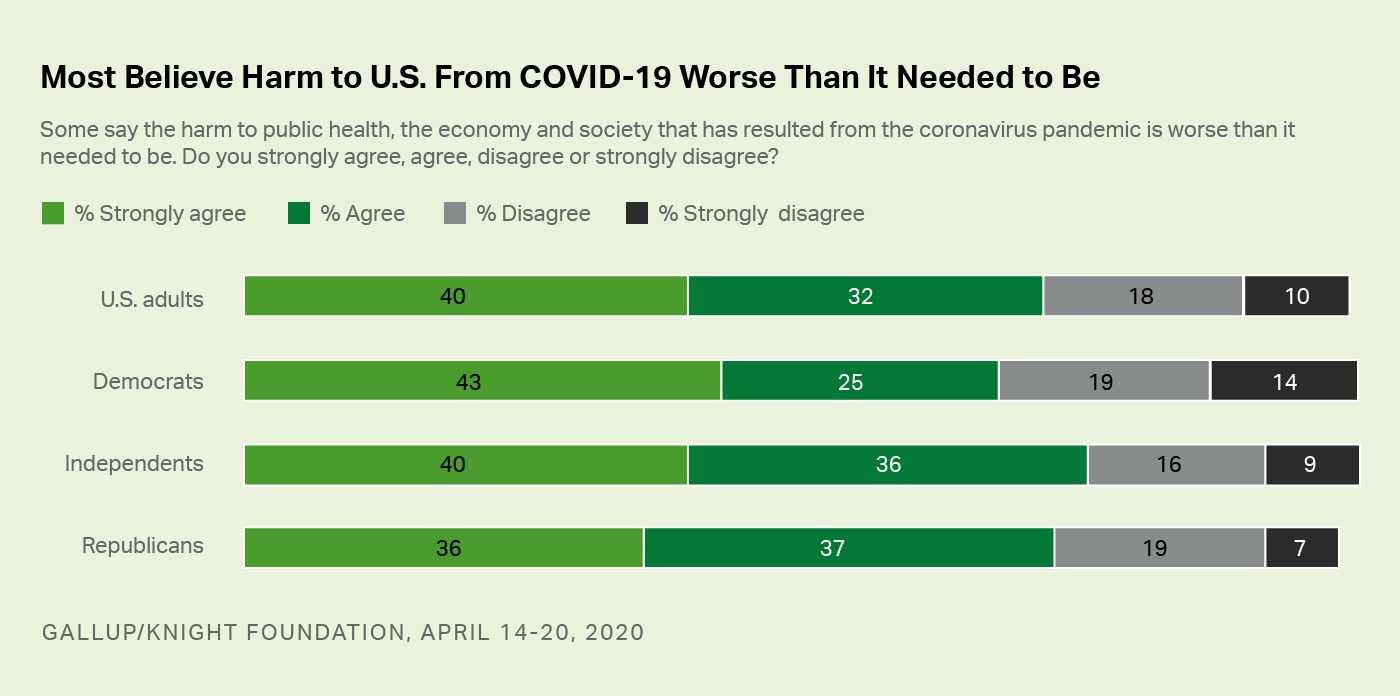

But let’s look at the remaining questions and results:

The third question is fairly straightforward: Was the pandemic more harmful to the US than it needed to be? Interestingly here the independents agree most, but pretty much everyone agrees that it was. But what I don’t see here is any particular assignation of blame. We also don’t see any attempt to define “harm.” Was the harm in terms of public health, or to individuals and the country? Do people believe the unnecessary harm was caused by media reporting, let alone exaggeration or down-playing? That’s not part of the question. What about a lack of solid information, down-played or exaggerated? Also not addressed. One might infer the Democrats think the harm came from downplaying, while Republicans think it was from exaggeration, but causation was never addressed in this question. People simply think more harm was done than should have been.

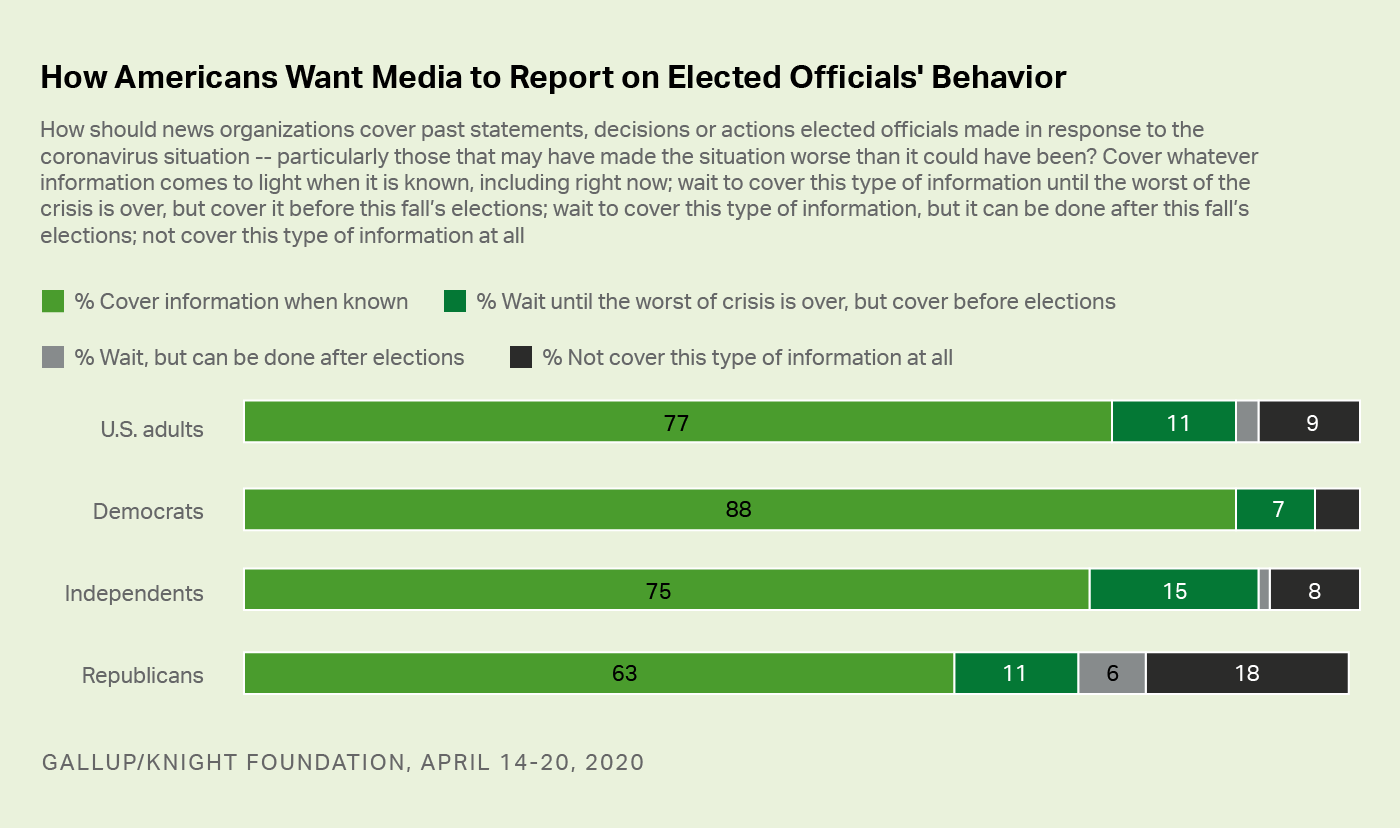

The last question is just kinda of weird. It asks how people want the actions of public officials and the effects of their decisions to be reported on. Not surprisingly, as Donald Trump seems to be the main central figure under the microscope much of the time, a very high number of Democrats want them covered now. But also a high number of Republicans want coverage now, as well. But really, what value do we derive from this question? Evidently pretty much everyone wants the media to cover the actions of public officials and the results of those actions. There’s nothing at all here about whether or not we trust the media to cover it fairly, or even if we want it covered fairly. There’s really nothing here to support the Washington Examiner’s supposition that we believe the media botched their coverage. Same for PJ Media’s claim that the poll shows the media is not performing well in the crisis.

Okay, thanks for sticking with me this far. The bottom line here is regardless of what I think of the validity of the poll, the pollsters themselves did not attempt to read anything into the data that wasn’t supported by the data. They did a decent job. Less admirable was the news media’s interpretation thereof. Both headlines and articles try to get more out of the data than is really there. I’m not entirely sure about the Examiner’s leanings, but a quick online search suggests they lean right. And the right tends to be convinced that the media is biased left and/or doing a poor job of unbiased reporting. While it’s amusing that we have media claiming the media is doing a poor job, it seems evident they’re claiming it with very little substance to go on here.

But if we weren’t aware of their bias beforehand it would be easy to assume that the PJ Media article’s assessment is correct because it echoes the Washington Examiner’s assessment. And since PJ Media quotes from the the Examiner, they invite us to not look any further, not even to read the Examiner’s article. We have to dig down two levels to find that both media outlets are creating something out of nothing.

As much as I hate to say it, because I’m basically a lazy man, to be a true free thinker we have to do our homework. To do otherwise is to be misled. And the world needs more true free thinkers.

Interest rates are really low right now–which is one of the reasons I lost my job at the beginning of the year. But my loss may also be my gain. Mortgage rates are also pretty low right now. I have about 24 years left on a 30 year mortgage, and the fact that I’ll be 74 when that’s paid off doesn’t sit well. Yes, I have other plans to deal with that, but I wouldn’t mind also doing something now. So I set out to find out if rates are low enough that I might actually benefit.

First of all I tried one of those internet loan sites. I didn’t get far before I quit. RocketMortgage wanted every bit of information needed to apply for a loan before I could even find out what terms I could get. I refuse to give out that much information until I know they’re really going to need it. Bye-bye, RocketMortgage. I went back to the brick-n-mortar reliables. Kinda.

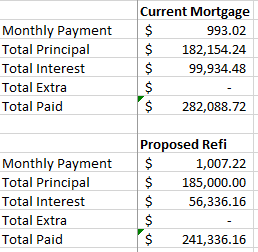

My current mortgage servicing company has been after me for a while now to see about refinancing (and adding on a home equity loan if they could talk me into it), so I decided to hear what they had to say. I wasn’t impressed. They could do a 20-year loan that would cost me about $300 more a month.

Then I called the local broker I went with the two previous times. He actually had access to a 20-year loan for a lower rate than most 15-years. The net increase would be about $17 a month. Now THAT could be doable. But…should I? Was I forgetting something? After all, there would be fees, which they would try to get me to build into the loan. Would it be worth it to cut only six years off my loan? Time to crunch the numbers!

Armed with my current rate, number of payments left, and my current principal and interest payments, was able to calculate the total interest over the remaining life of the loan. That came to just under $100,000. I then calculated the total interest I’d pay on the proposed 20-year loan (figuring in financing the refi-fees, which I likely won’t do). That came to just over $56,000. Not a trivial difference! But I’ve heard that it can sometimes work to your advantage to pay extra principal on your loan to get it paid off sooner. I decided to look into that, even though at this point I’m not sure I would really want to take that money from other projects to do so.

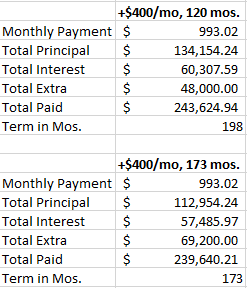

I played with several different models. I first tried applying $100 per month toward principal and discarded that option. It barely moved the needle. Increasing the pay-down, I found that if I paid an extra $400 a month toward principal for first 120 months I could get the total outlay on my current loan down to about $23000 more than I’d pay with the 20-year, and pay it off 42 months earlier–in just over 16 years instead of 20. And if I paid $400 a month for 173 months I’d have it paid off entirely–in around 14 years. That would be right before I hit retirement age–good timing!

But wait. Assuming that’s even $400 I have, I’ve also had people tell me it would be better to put that money into an investment that earns higher interest instead, have it build up faster, and use that to pay the mortgage off early. In any case, in my MBA program they taught us that when looking at any project you should compare what they called the “opportunity cost,” or what you might lose with this option over some other bench-mark option, such as a long-term fixed-return investment. You might do well with this option, but what if you did something else with it instead?

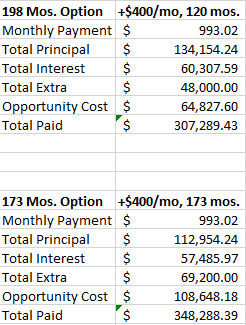

My financial advisor usually tosses around 6% as a fairly safe rate of return on long-term investment-i.e. bond funds with little to no risk, so I used that to calculate how much I would have if I invested the same $400 a month for the same length of time. In the 198-month scenario, where I put in $400 a month for 120 months I would have $64,827. In the 173-month scenario, investing $400 a month for 173 months, I’d have $108,648. Compared to my proposed refinance, by paying down my mortgage I’d be losing the additional principle I paid, but also losing the gains I might have realized by investing it. It’s something of a double-whammy.

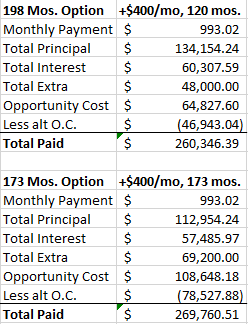

But wait again. In both those scenarios I would be done making mortgage payments earlier than if I went with the 240-month refinance. Being done sooner would mean I could turn that $1007 monthly payment toward investments. What about the opportunity cost of that money? More quick calculations, and under the 198-month scenario, investing my monthly payments for those 42 fewer months, it would come to $46,943, and in the 173-month scenario, investing for 67 months, it would be $78,527. If we put that back into the picture we end up with a significantly smaller gap from the $241,336 total paid out on the 240-month refinance; about $19,000 to $28,000.

Of course these two scenarios really do depend on the availability of the $400 a month to apply toward principle. The opportunity cost is real, as the only prospect for finding that money would be to take from what I’m currently saving each month to invest. The savings in interest doesn’t keep up with the amount put in to pay down the principle, let alone with the interest earned on investing it.

Bottom line: My 20-year refinance would save me about $40,000 over paying out the rest of my 30-year mortgage, and about $19,000 to $28,000 over money-to-principle scenarios. The value of investing that proposed extra principal payment early on (i.e. over a longer period) is hard to beat, even versus a shorter term but larger amount later. Slow and steady wins the race, but more money up front gets you there even faster.

While the over-all benefits aren’t as high as I had hoped, in this case, the value of refinancing is pretty clear. I save four years and about $40,000, plus I get to take that proposed added principal payment (I still don’t now if I could swing that), and invest it at at least twice the rate of what I pay on my loan. I’d have to say it’s worth it to refinance.

Of course I’m no financial adviser, I haven’t given you all my details here, and I don’t know your circumstances. This isn’t really meant to tell you whether or not you might benefit. This is primarily an exercise to help you evaluate for yourself. Just remember to look at all angles, not just the most immediate. I probably missed something here, too, but I’m going into this much more sure of what I’m doing than if I had simply thought, “Four fewer years is always a good thing, right?”

Ashley over at YouNeedABudget.com brought up an interesting motivational concept in her recent video. Citing someone else’s comic, she talks about doing things for our future self such as, if you know you need to do a video shoot in the morning, making sure your camera batteries are charged and your memory cards are wiped the night before so that’s one less thing to have to deal with in the morning. Take a look (no prior knowledge of YNAB required):

As I watched the video it occurred to me that this idea of taking care of your future self is at the heart of self-reliance. Building up some food storage and your savings is a terrific gift to your future self who is out of work for a few months, or laid up on temporary disability. Taking a few extra online classes in your field or exploring a related field may be just the thing to help future you really nail an opportunity at work. Always taking the time to make sure you keep your car’s tank at least half-filled will be greatly appreciated later when something comes up on the day you usually fill up and you have to go another day or two before you get another chance.

The essence of self-reliance is making sure your future self has very little to worry about. It can even start with the smaller things that Ashley mentions, but dealing with things now instead of later will definitely make future you want to thank you!

Ken Jorgustin at Modern Survival Blog takes up the question of whether it’s worth it to invest in self-reliance. He looks at various types of home production, such as raising your own chickens, growing your own garden, or even switching to solar energy all cost money, and often those same products can be obtained commercially for less.

During the process of building their palace, I’ve thought about the money it took to get this done. As well as the ongoing costs of maintaining the small flock, and feeding them. Let me put it this way. You might get depressed to realize the ultimate cost per dozen eggs output compared to the money input!

Ken Jorgustin

I’ve noticed that with gardening. In both places we’ve lived our irrigation and gardening water comes from the same water as our culinary and hygienic water, and the cost can more than double during the summer months. Whatever money we save by growing our own vegetables is more than eaten up in the water, seeds, tools, and fertilizer needed to grow them. We ultimately decided it simply wasn’t worthwhile to try to grow our own potatoes in Idaho.

We also looked at solar power ourselves a few years ago and realized that in spite of what the salesman told us, the system would never pay for itself, even if the power company paid for any excess electricity we generated–which they stopped doing within a few years. While we would like to have been able to do more to reduce pollution and our own energy dependence we just couldn’t justify the expense.

It can all be enough to make you step back and wonder if it’s really worthwhile to take a different path. But, as Jorgustin explains, the answer will be different for everyone. For some people cost is the only consideration, and they’ll likely not bother with many self-reliance measures. For my wife and I, we find home-grown food is usually healthier and better tasting. What’s more, there may be rough times ahead–times when the stores won’t be able to get the stock they usually get. We may very well need to supplement our food supply from our own yard. In the middle of the crisis is not the time to be learning what grows and what doesn’t, or how to lay out your garden, your watering, etc. And as we’ve seen, the price of things can increase quickly when it’s in short supply.

A considerable part of self-reliance, and especially emergency preparedness, is not just having the things you need when things go wrong, but knowing what to do with them. Maybe not everything we can do we should do, but it is worthwhile to consider what things you want to be able to do. And sometimes it just feels good to do it.

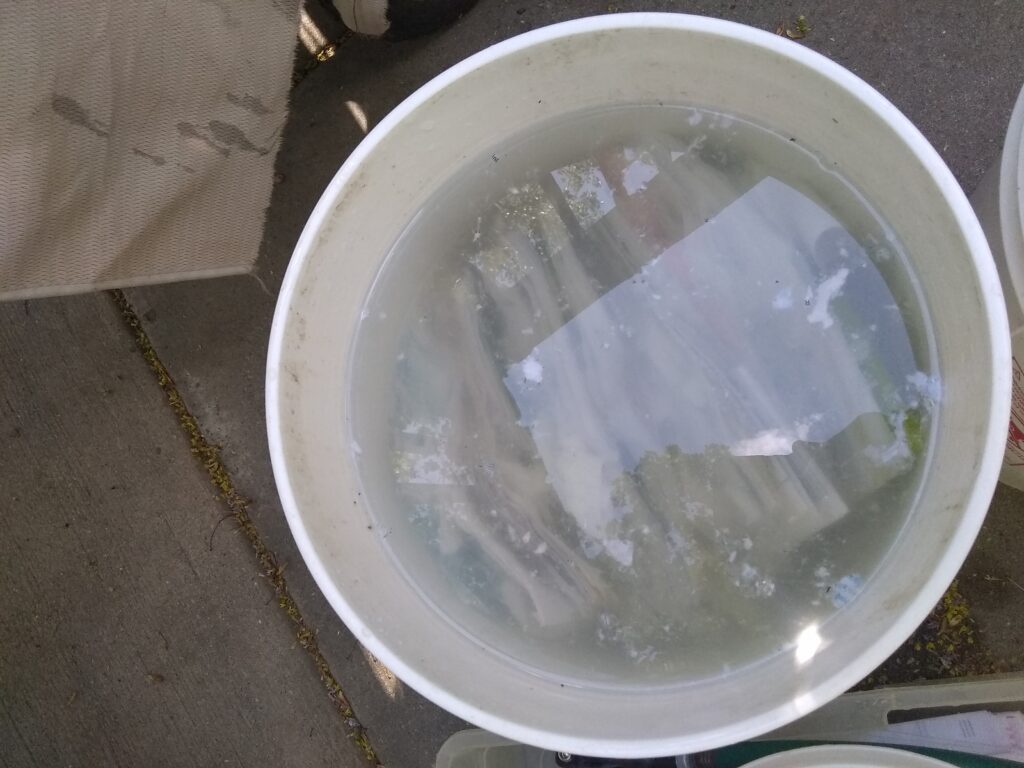

I am hard on paper shredders. I’ve destroyed two of them in the past year. I like to think it’s just because those diamond-cut shredders are flimsy, but I suspect it’s really because I push the limits a little too often. In any case, I recently cleaned out the shed and found I had three boxes full of old financial docs, dating back twenty years. That’s way longer than I need, and is perhaps even becoming a liability. But…I don’t have a shredder.

My wife suggested I look up other ways of destroying documents, so I did. I don’t think a burn-barrel would go over too well these days, but a soak barrel sounded interesting. The idea is to get a bucket of water and dump your documents in there, let them soak, then stir them well to break them up and turn them to pulp. Then you pour the pulp out somewhere and let the water drain/soak/evaporate out of it until it hardens up. You can then pick it up and put it in the garbage, and no one will really be able to get any info out of the mess.

So I tried it. I immediately got it wrong. I started by filling two five gallon buckets with papers. Then I filled them with water.

Do you ever cook spaghetti only to have the noodles all clump together tightly and not want to separate? Paper is much, much worse. I should have separated them more, or better yet filled the bucket with water first, then put the documents in, page by page until it was maybe half full. The first time I went to stir them they all stuck together in a single mass that wouldn’t budge, let alone break up. Even my hand tiller tool, used for breaking up garden soil, wouldn’t work.

It became a battle of wills. I’d go outside once or twice every day, replace any evaporated or soaked-in water, and stir/till each bucket, slowly scraping bits and pieces of paper from the clumps. Over about a week it began to look more promising.

Finally I could wait no longer, and dumped out the two buckets on a tarp I set up and spread the pulp out to dry. That didn’t go quickly, either, as we have very few sunny places in our yard. It probably took another week of drying.

Eventually it dried enough to make an interesting piece of art. My wife joked about using them for floor mats, or table placemats, or finding a way to roll it out thinner and making our own recycled paper. Frankly, I don’t think there’s much worth doing with it other than throwing it away.

I really don’t see much to recommend this particular approach to document destruction. At this rate I’ll have my documents destroyed around about….October. It’s cheap, and it may even be less labor-intensive than sitting there for hours feeding a few pages at a time through a shredder. It’s certainly cheaper than a new shredder. What I really ought to do is get a good document scanner and a good shredder, scan the documents as soon as I get them and shred them on the spot. But I’m a cheapskate, so that probably won’t happen. But I also won’t pay to have the local UPS Store dispose of them for me, either, so who knows. Maybe the pulp-pots will remain in business?

I’ll probably try another batch with an entirely different approach and see how that goes, but at least by the time I’ve done that it should be easier to justify shelling out more for a good, industrial-strength shredder.

I went to post a link to yesterday’s column on Facebook and suddenly realized I’d gotten sidetracked when I wrote it. The post title had nothing to do with what I ended up writing about! So here I am, back again, hoping to get it right this time!

As I began yesterday, the article “7 Tips For Increasing Self-Reliance” lists some of the usual things and some less-than-usual. One that perhaps doesn’t get the attention it deserves is their point on looking after your body:

While you shouldn’t expect yourself to be your own doctor and should always seek medical advice if you are concerned about your health, try to look after your body to minimize the need for treatment and medication.

While you shouldn’t expect yourself to be your own doctor and should always seek medical advice if you are concerned about your health, try to look after your body to minimize the need for treatment and medication.

Work out on a regular basis and eat healthy food most of the time. Try to stay informed about specific diseases that you may be at risk of developing (whether genetic or environmental reasons). All of these actions will make you more confident about relying on your body. It will have the side-effect of making you feel more comfortable with the idea of self-reliance in general.

I’ve always taken my health for granted. Somehow I bucked the family genetic trend and was born with a high metabolism, I’ve been on the skinny side most of my life. While never all that physically active, I was certainly more so than most teens today. And in college I was in great shape; slinging a vacuum around a department store for four hours every morning, followed by frequent, high speed walks back and forth from upper campus to lower. I never considered my body; it always did what I needed it to do.

Then I graduated and got a desk job. And I got married. In a short amount of time I put on thirty pounds. My doctor got on my case about that, and with little modification I took those pounds back off. Then I found that fat had been masking something else. I had a heart murmur. We quickly discovered I have two leaky heart valves. Fortunately, it was nothing serious yet, so we continued to monitor it. My lifestyle still didn’t change much.

When we moved to Utah I didn’t even continue monitoring it for a while. And when I finally did, things seemed normal. Then suddenly, one year, they weren’t. My heart is getting worse. Though getting in better shape can’t fix that, the doctor agreed it certainly wouldn’t hurt. So I’ve been making a more concerted effort to get in better shape.

Mind you, I still find exercise an inconvenience. There are other things I’d much rather do than spend an hour a day (on average) exercising. But I will grudgingly admit to noticing a difference when I do. I’m not as tired. I don’t give out as quickly. I can pretty much do whatever I need to do around the house

Part of the trick for me is to either find something I enjoy doing, or find ways to make what I’m doing enjoyable. I ride a stationary bike every morning for 25-30 minutes. I listen to speakers or audio books during that time so that I pay less attention to the clock. Every other day I practice basketball, either playing with my son or working on my shot on my own. Since my objective is completely separate from the exercise I don’t focus on the fact that I’m exercising.

I’ll never been one of those guys who measures his exercise in miles our hours. Spending six hours on a Saturday biking 50 miles just doesn’t sound fun to me. For me the primary motivation comes down to this: I’ve got a heart condition that could significantly limit my life span. My best chance of beating that is by being as healthy as I can. Life is only getting more interesting the older I get. I don’t want to miss anything.